Shenzhen 9610 no ticket tax exemption landing: three types of sellers fate divergence, some people carnival someone out of the game

Published: 2026-04-10

On February 1, 2026, Shenzhen 9610 Tax Free Registration Module was officially launched. As soon as the news came out, the cross-border circle instantly exploded - some people declared that ”zero cost to the sea, profits all in the bag”, while some people calmly pointed out that ”tax-free ≠ save money, choose the wrong instead of losing more”. In this article, we will put the most core things at once to say through!The

Summary of this article:

I. What's Happening? A policy background compendium

Second, what exactly is exempted from taxation without a ticket?

Three types of sellers with very different fates

IV. A table showing the four modes of exports

V. Operational process: five steps to complete the registration of tax exemption without a ticket

VI. Five ”minefields” under the 9610 model”

VII. Should I go ticketless tax-free? Do this multiple choice question first

"one" radical in Chinese characters (Kangxi radical 1),What's Happening? Policy Background Sorting

Let's get one thing straight first: what's coming online this time in Shenzhen is not a new policy, but a new tool.

“The matter of ”no ticket tax exemption" was mentioned in the policy of the comprehensive test zone as early as 2018. The core reason why almost no sellers have really landed in the past few years is that there is no digital registration interface - there is no connection between customs, tax, and the system, and enterprises simply don't know how to declare.

On January 31, 2026, the Shenzhen Bureau of Commerce officially announced that the 9610 registration module for cross-border e-commerce ”no ticket, no tax” had been optimized and upgraded.Official online operation from February 1. Shenzhen has thus become the first city in the country to actually open up this route.

📌 What is ”9610″?

9610 is the customs supervision code, full name ”cross-border trade e-commerce”, for the B2C small parcel direct export mode - that is, the seller packaged goods, through the international courier / small parcel channels directly to overseas consumers. amazon Amazon, FBM, Wish, eBay and other platforms, self-shipment sellers, as well as independent station sellers, often use this model.

So that's something to keep in mind:Shenzhen 9610 duty free without ticket, only applicable to Shenzhen registered sellers + 9610 parcel direct mail business, other modes (9810 Overseas Warehouse, 0110 General Trade, etc.) are out of scope.

二,What exactly is exempted from the no-ticket tax exemption?

Many people confuse ”no invoice tax exemption” and ”export tax rebate”, which is the biggest cognitive misunderstanding.

The essential difference is clear in one sentence

Export Tax Refund = you pay the tax up front and get it back from the government (requires an invoice) No invoice = you don't have to pay tax at all, you don't need an input invoice to export.

Under China's current value-added tax (VAT) system, cross-border e-commerce exports are usually treated as ”exempted from VAT” or ”exempted from tax refund”. Theoretically, exported goods are exempt from VAT - but in practice, there is no input invoice, the tax system can not be written off, and enterprises are often faced with the dilemma of ”not being able to prove that the tax has been transferred out”, either according to the domestic sales of the tax, or the accumulation of tax risks.

Shenzhen 9610 Tax exemption without ticket.

: Input invoices are not required and exports are recognized directly as exempt.

🅰️ Applicable to: small and medium-sized sellers without input invoices, or insufficient invoices

⚠️ important cost: input tax is not deductible and you can't claim a refund, you can only choose one or the other!

surname San,Three types of sellers with very different fates

Shenzhen 9610 tax exemption without a ticket is definitely not a policy dividend ”for everyone”. Based on the comprehensive analysis of multiple sources, the following three types of cross-border sellers will face a completely different situation:

1,Benefits the most ✅

Small and medium-sized sellers with sporadic purchases and no ticketed sources of goods

The typical image of this kind of sellers is: they take goods from 1688 and wholesale market, the suppliers are unwilling or unable to provide VAT invoice, the procurement cost is low but the tax treatment is confusing. If you go for tax exemption without invoice, you can say goodbye to the risk of ”gray settlement” and ”frozen card”.

Recommendation Index: ⭐⭐⭐⭐⭐ Highly Recommended

2,Need to do the math carefully ⚖️

Medium to large sellers with regular suppliers and access to invoices

The problem for this type of seller is that if you could have gotten an input invoice with a 13% tax rate, the amount of tax refund you could have gotten by taking the export tax rebate could have been much higher than the amount of tax you would have saved by being ”tax exempt”. Tax exemption may seem simple, but giving up the right to a tax refund means giving up the real benefit.

Recommendation: do the math before deciding

3,Largely irrelevant ❌

Sellers who take 9810 overseas warehouse mode or general trade 0110

Shenzhen 9610 no ticket duty free is limited to 9610 parcel direct mail. Sellers going to overseas warehouses (FBA/Overseas Warehouse) use 9810 code, sellers in Yiwu/Guangzhou, etc. go to 1039 Market Purchase Trade - these are not covered by this policy.

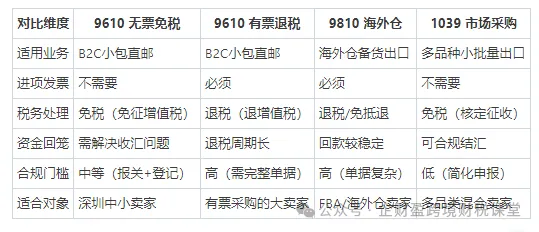

四,A table of the four export modes

五,Operation process: five steps to complete the registration of tax exemption without tickets

Step 1: Confirmation of subject matter eligibility Verify that the enterprise is registered in Shenzhen and is actually using the 9610 model for customs clearance for export.

Step 2: Complete the cross-border e-commerce enterprise filing at customs (if not yet completed) to obtain a cross-border e-commerce qualification.

Step 3: Login to Shenzhen E-Port/Related Systems Find the ”9610 Registration for Tax Exemption without Invoice” module and submit the basic information of the enterprise and business description.

Step 4: Accurately fill in the seller's unified social credit code when declaring customs clearance Ensure consistency with registration information, which is the key field that triggers the tax exemption.

Step 5: Keep a record of the transaction for your records Including order information, payment records, logistics documents (”three single comparison”: order/payment/logistics), preserved for a period of not less than 5 years.

6(math.) genusFive ”minefields” in the 9610 model”

Any policy dividend has a corresponding risk boundary. The following are the generally recognized high risk points of the 9610 model across the realm, which must be avoided in advance:

⚠️ Minefield 1: Customs declaration information does not match the reality

Misrepresentation of seller information (e.g., replacing it with other enterprise codes), understatement of the value of goods, and indiscriminate filling in of HS codes - once compared with anomalies by the Customs big data system, it is a minor case of back taxes and fines, and a serious case of criminal liability involving fraudulent tax exemption preferences.

⚠️ Minefield 2: There's no turning back from choosing the wrong tax path

Once you have opted for the no-invoice tax exemption, it means that you have given up your right to input tax credits and refunds. If you find out after the fact that it is more cost-effective to go for a tax refund, you cannot go back and retroactively recognize it, and you can only start adjusting it from the new business after you have chosen it.

⚠️ Minefield 3: Non-compliance of foreign exchange collection channels

Tax-free, but how to get the money back? Some sellers have long relied on underground money changers or personal accounts to collect foreign exchange, which poses serious risks of ”card freezing” and anti-money laundering compliance.

⚠️ Minefield 4: Neglecting the three-sheet comparison retention

9610 tax exemption is not ”reported on the line”, the tax and customs will regularly check whether the ”order-payment-logistics” three single real match. False orders or single brush behavior, even if the customs declaration can not escape the data verification.

Shenzhen is currently the only city where the registration module is officially online. Sellers in other cities who want to enjoy the same treatment need to wait for their local systems to go live. Guangzhou, Hangzhou and Shanghai have not yet followed suit.

七,Want to go ticketless tax-free? Do this multiple choice question first

The central question that many people struggle with is: go tax-free without a ticket, or go with a refund with a ticket? A framework for decision making is given here:

If your annual sales × applicable tax rate > cost of refund agent → choose refund

Example: annual sales of $5 million, purchase costs of $4 million (all inclusive of tickets), tax refundable amount of about $520,000 (13%), minus agency fees and still have a net gain → tax refund is more cost-effective.

If you are unable to obtain invoices for the majority of your purchases → select Tax Exemption Without Invoices

Example: a large number of purchases from 1688 without tickets, or take goods from the wholesale market, the accounts are chaotic, the tax risk accumulates → No ticket tax exemption allows you to be completely compliant, say goodbye to the risk of freezing card.

There is another smart approach: separation of the main body - ticketed business goes to company A (tax rebate), non-ticketed business goes to company B (tax exemption), and the two lines run in parallel to maximize the benefits. Of course, this requires a professional tax team to design the structure.

八,The dividends are real and so are the pits

Shenzhen 9610 tax exemption without a ticket is a milestone policy landing in the process of cross-border e-commerce tax compliance. It allows a large number of small and medium-sized sellers have ”not rely on gray channels can also be normal export” path. But the policy is again friendly, but also can not hold ”do not understand the rules on rushing in” the price.

Photo credit: Beanbag

Contact: kuajinghg001

The article is for reference only, please consult your professional advisor for details

Tags:

Financial and tax risk treatment

9610

Cross-border e-commerce compliance

tax planning

E-commerce compliance

cross-border e-commerce

Recommended

Cross-border e-commerce B2B must see! Registered Hong Kong company stationed in the Ali International Station, really fragrant!

In today's globalized business environment, the cross-border e-commerce B2B model is rapidly emerging with its unique advantages. For many enterprises engaged in cross-border trade, choosing a suitable platform and registering an advantageous company are undoubtedly the key keys to open the door to the international market.

2024 Hong Kong Company Account Opening Tips! How to choose the right Hong Kong bank account?

Global anti-money laundering regulations are becoming more and more stringent, the banks to maintain an account of the sunk cost is getting higher and higher, not moving hundreds of millions of dollars in fines, so that the major banks to open an account threshold as well as the audit process high up, already have a Hong Kong company bosses, how to choose the Hong Kong bank to open a public account? How much does it cost and how to operate? Today to give you a detailed introduction to the Hong Kong company account how to choose, as well as the approximate costs required and other content.

Hong Kong company registration advantages + registration conditions + registration process to share!

If you want to start a business and develop overseas markets, registering a Hong Kong company is undoubtedly a very forward-looking choice. With its unique geographical location, sound legal system, low tax rate and open business environment, Hong Kong company has become a "sharp weapon" for many business owners to open up overseas markets. Why is it so important to register a Hong Kong company in 2024?