Hong Kong offshore exemption tax avoidance dream shattered?2026 strict examination + mainland tax recovery, 90% sellers are wrong!

Published: 2026-05-19

In cross-border e-commerce and foreign trade circles, “Hong Kong offshore exemption” had been regarded as a “tax avoidance magic weapon” - many sellers thought that by registering a Hong Kong company and applying for an offshore exemption, they would be able to realize Hong Kong, mainland “two tax exemptions”. However, in 2026, the Hong Kong Inland Revenue Department (IRD) tightened its scrutiny, superimposed on the upgrading of the Mainland's CRS information exchange and Golden Tax System.The era of offshore exemptions for tax avoidance is over for goodThe

To receive information + quotation, please contact me (WeChat/telephone inquiry: 1304348584).

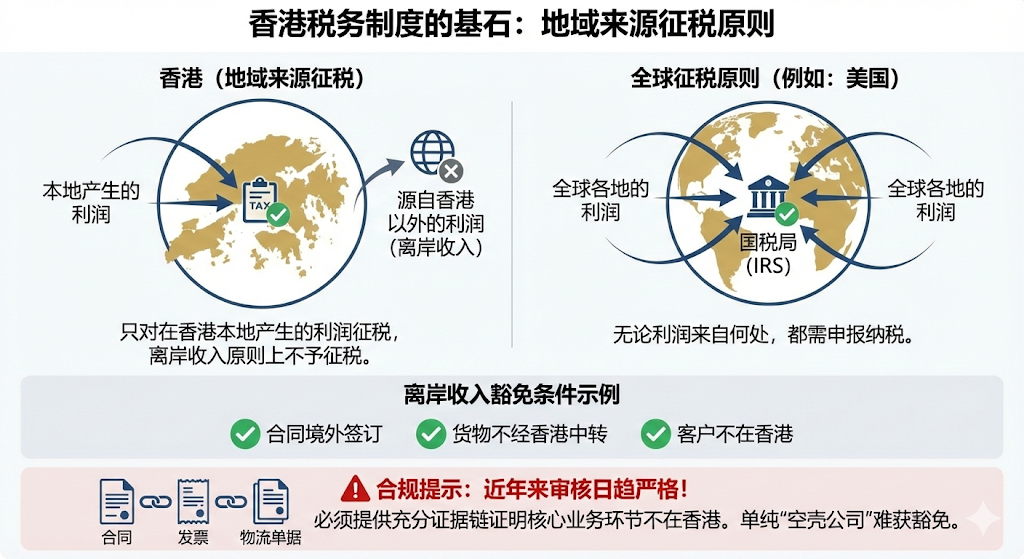

I. The core logic of offshore exemptions: not “tax exemption” but “source taxation”

Hong Kong is practicingPrinciple of territorial source taxationThe offshore exemption is an exemption from Hong Kong profits tax, which is only levied on Hong Kong-sourced profits (8.25% for the first HK$2 million of profits and 16.5% for the excess). The essence of the offshore exemption is to prove to the Hong Kong Inland Revenue Department thatProfits are derived entirely from outside Hong Kong and have no material connection with Hong KongIn addition to the above, the Government is also required to provide the following information: (a) the amount of profits tax payable in respect of the

However, many sellers misinterpret this to mean that “you don't have to pay tax if your application is successful”, but in factThe exemption is for Hong Kong tax, not Mainland taxThe profits will ultimately have to be declared at the place of actual operation (e.g. the Mainland). Profits will ultimately have to be declared for tax purposes in the actual place of business (e.g. the Mainland), and it is totally unrealistic to grant tax exemption at both ends.

II. 2026 Offshore Exemption Application: Extremely High Threshold, 90% Cross-Border Sellers Fail to Meet the Standard

Hong Kong Inland Revenue Department (IRD) 2026 review is fully upgraded to require “Fully offshore, zero Hong Kong connection”, any part of which involves Hong Kong, the application is rejected outright.

1. Five mandatory conditions, one without the other

✅Transaction Full Process Offshore: Contract negotiation, signing, order processing and pricing decisions are all done outside Hong Kong with no local Hong Kong involvement.

✅Cargo flow without Hong Kong: The goods are shipped directly to overseas, not through Hong Kong warehousing and transshipment, the bill of lading and customs declaration need to be clearly marked “no Hong Kong transit”.

✅Partner has no Hong Kong connection: Customers and suppliers are non-Hong Kong enterprises or individuals, with no Hong Kong shareholders or partners.

✅No physical traces of Hong Kong: Do not set up offices or warehouses in Hong Kong, do not employ Hong Kong staff, and do not allow directors/core executives to stay in Hong Kong for more than 60-90 days per year.

✅Offshore flow of funds: Payment and receipt of goods and approval of funds are done outside Hong Kong, and the Hong Kong account is only for administrative receipts and disbursements and does not retain funds.

2. Cross-border sellers are naturally difficult to meet standards

The vast majority of cross-border sellers have their actual operation team, procurement supply chain, and decision-making center in the Mainland, and their goods are often transshipped through Hong Kong, and they even use Hong Kong accounts to receive payments frequently. TheseTraces of operation in the MainlandAs a direct result, the “complete offshoring” requirement cannot be met and the application is highly susceptible to rejection.

Third, the difficulty of the operation is full: it takes 1-2 years, high cost, the success rate plummeted.

Even if the basic requirements are met, the application process is challenging and costly in both time and money.

1. Complex processes and long lead times

The application requires a Hong Kong company audit before submitting an application for exemption to the Inland Revenue Department, during which a large number of documents, such as business certificates, logistic documents, capital flows, etc., need to be supplemented.Overall 1-2 years, and are subject to annual application and annual review.

2. Tightened scrutiny with the addition of the “foreign tax clearance certificate” requirement

Under the new rules in 2026, the Hong Kong Inland Revenue Department (IRD) has made it mandatory for the provision ofProof of tax payment at the source of profitIf the information is not available, the application will be rejected directly and required to pay back Hong Kong taxes and late fees. Meanwhile, IRD will penetrate to verify the authenticity of the business, and false materials will be directly blacklisted, affecting all subsequent tax applications.

3. Accountants are costly and pay for failure

The application requires full assistance from a licensed accountant in Hong Kong, with a basic service fee of tens of thousands of Hong Kong dollars, or higher if the business is complex.Even if the application is unsuccessful, the audit and service fees incurred will not be refunded., a double loss of time and money.

Fourth, the fatal hidden risk: exemption success, but instead triggered a huge amount of back taxes in the Mainland

It's the most overlooked minefield--Successful application for offshore exemption does not mean tax compliance, but may lead to tax audits in the Mainland.The

1. CRS information exchange with full data transparency

Hong Kong is a CRS participating region, and will regularly provide information on account flows, earnings, and exemption applications of Hong Kong companies.Automatic exchange to the Mainland Inland Revenue Department. The Mainland's Golden Tax System can pinpoint enterprises with “undeclared offshore income” through data matching.

2. Three major tax consequences with significant losses

✅Recognized as a Mainland tax resident enterprise: If the company's actual management organization is in the Mainland, it is subject to corporate income tax at the rate of 25%, and worldwide income is required to be declared.

✅Constituting a permanent body in the Mainland: Mainland operating teams, office premises or long-term business activities will be recognized as permanent establishments and profits will be subject to full tax in the Mainland.

✅Diverted Profits Audited: If the profit of a Hong Kong company is significantly lower than the industry level, or if it understates its income for a long period of time, it will be recognized as “transferring profits to avoid tax” and faceBack taxes + late fees + penaltiesThe maximum amount is five times the amount of the tax.

V. Pragmatic Compliance Path for Cross-border Sellers: Abandon Offshore Exemptions and Standardize Taxation

Blindly applying for offshore exemption is not worth the loss, and complying with the law is the long-term solution. The following three paths can optimize tax burden and prevent and control risks:

1. Facing up to the operation of the Mainland and complying with the reporting requirements

Give up the illusion of “offshore tax exemption”, Hong Kong companies by the rulesNormal tax filing(no application for exemption), mainland entities declare their incomes truthfully and enjoy preferential policies such as small and micro enterprises and export tax rebates.

2. Good transfer pricing and rational allocation of profits

If there are connected transactions between the Mainland and Hong Kong, there is a need to formulateRational transfer pricing policy, to ensure that profits are reasonably distributed between the two places and to avoid being recognized as “transferring profits”. At the same time, retain complete contracts, invoices and logistics documents to prove the authenticity of the transaction.

3. Optimizing corporate structures and reducing tax liabilities

✅Mainland subjects: registered as small-scale taxpayers (annual sales ≤5 million), enjoying quarterly 300,000 VAT exemption; or upgraded general taxpayers, enjoying export tax rebate.

✅ Hong Kong company: only as the main body of the collection and branding, not actually operating, according to the Hong Kong low tax rate (8.25%-16.5%) normal tax, to avoid the large amount of profit stagnation.

concluding remarks

In 2026, Hong Kong's offshore tax exemption has changed from a “shortcut to tax avoidance” to a “high-risk trap”. Under the triple pressure of strict audit policy, high cost, and Mainland CRS audits, the90% None of the cross-border sellers are suitable for applicationInstead of taking risks, we should focus on tax compliance. Instead of taking a risk by chance, it is better to face up to tax compliance -- normal tax filing for Hong Kong companies, standardized declaration for mainland subjects, and good transfer pricing and voucher retention can avoid the risk of back tax penalty and optimize tax burden through tax incentives. Compliance is not a cost, but a “lifeline” for cross-border business. The only way to achieve long-term stable development is to build a strong tax defense.

If you want to understand the Hong Kong company registration or for Hong Kong offshore exemption related policies, welcome to scan the following two-dimensional code (WeChat / telephone contact can be) at any time to contact us, we will create the most suitable program for you!

To receive information + quotation, please contact me (WeChat/telephone inquiry: 1304348584).

Tags:

Hong Kong Dollar

Hong Kong Company Compliance

Hong Kong offshore exemption

Hong Kong Company Registration

Hong Kong company

Hong Kong Company Registration

Recommended

Cross-border e-commerce B2B must see! Registered Hong Kong company stationed in the Ali International Station, really fragrant!

In today's globalized business environment, the cross-border e-commerce B2B model is rapidly emerging with its unique advantages. For many enterprises engaged in cross-border trade, choosing a suitable platform and registering an advantageous company are undoubtedly the key keys to open the door to the international market.

2024 Hong Kong Company Account Opening Tips! How to choose the right Hong Kong bank account?

Global anti-money laundering regulations are becoming more and more stringent, the banks to maintain an account of the sunk cost is getting higher and higher, not moving hundreds of millions of dollars in fines, so that the major banks to open an account threshold as well as the audit process high up, already have a Hong Kong company bosses, how to choose the Hong Kong bank to open a public account? How much does it cost and how to operate? Today to give you a detailed introduction to the Hong Kong company account how to choose, as well as the approximate costs required and other content.

Hong Kong company registration advantages + registration conditions + registration process to share!

If you want to start a business and develop overseas markets, registering a Hong Kong company is undoubtedly a very forward-looking choice. With its unique geographical location, sound legal system, low tax rate and open business environment, Hong Kong company has become a "sharp weapon" for many business owners to open up overseas markets. Why is it so important to register a Hong Kong company in 2024?