Cross-border sellers "compliance storm" is coming, quickly look at the four survival guide! How to achieve tax compliance for cross-border enterprises in 2026!

Published: 2026-02-25

Enterprise Caiying Group provides U.S. companies / Singapore companies / Japanese companies / Thailand companies / Malaysia companies / Canada companies / Mexico companies / Brazil companies / British companies / France companies / New Zealand companies / Vietnam companies / Indonesia companies / Dubai companies and other foreign companies registered in the relevant business and taxation services, but also to provide Hong Kong companies / Shenzhen companies / Guangzhou companies / Shanghai companies / Hangzhou companies / Beijing companies / Hainan companies and other domestic companies registered corporate services, company annual audit / bookkeeping tax / payment of MPF / change information / bank account opening / ODI filing / BVI registration / tax compliance / cross-border e-commerce accompanied by running on behalf of the corporate services. Company / Hainan company and other domestic companies registered corporate services, company annual audit audit / bookkeeping and tax returns / payment of MPF / change of information / bank account opening / ODI filing / BVI registration / tax compliance / cross-border e-commerce accompanied by running on behalf of the operation of the enterprise one-stop service, you have the need or interested in any time to drop me (phone and WeChat consulting: 13045886252).

The cross-border e-commerce community is experiencing a "compliance storm". 2026 January 1, the new "People's Republic of China Value-added Tax Law" is officially implemented, breaking the industry's long-standing "buffer period" protection.

According to the analysis of the authoritative tax agency, the new regulations bring about theInstant recognition of general taxpayers and sales retrospective mechanismTwo major adjustments are instantly transferring compliance pressure to every cross-border seller's books.

The Collective Dilemma of Cross-Border Sellers as New Laws Strike

The cross-border e-commerce world has been permeated by a tense atmosphere recently. With the new VAT law of 2026 coming into force, many practices that had been teetering on the edge of taxation are facing unprecedented challenges.

"Last week we accounted for our annual sales and realized that we had exceeded the $5 million red line. According to the new regulations, we immediately became a general taxpayer, and the previously planned buffer period is completely gone." An Amazon seller who specializes in household goods said helplessly.

Data from the State Administration of Taxation (SAT) shows that the number of comprehensive cross-border e-commerce pilot zones across the country has reached 165, covering 31 provinces. Among the millions of sellers in these pilot zones, as many as 30% have annual sales close to the $5 million red line.

This means that the new tax law adjustment will directly affect a large number of growing cross-border e-commerce enterprises.

01 Comparative analysis, the three core differences between the old and new regulations

The differences between the old and new VAT laws in the cross-border e-commerce sector are mainly in three areas. Understanding these differences is the basis for developing a response strategy.

(1) general taxpayer recognized changes in standards: the old regulations, annual sales of more than 5 million yuan, sellers have nearly a month of "buffer" to adjust business and financial arrangements. The new rules provide that once sales exceed the red line in the current period, the effective date of the general taxpayer for the exceeding the standard of the current period on the first day, no longer the previous "effective the following month"!

(2) Adjustment of sales retrospective mechanism: In the past, concealed income discovered by tax audits was usually included in the current period of adjustment. The new regulations require that all adjusted sales be backdated to the period in which the original business occurred. This change means that back taxes on historical income may face higher tax rates and late fees.

(3) Calculation of the accounting cycle: The old law allowed sellers to "reset" 12 months of cumulative sales by suspending operations. Under the new law, 12 consecutive months or four consecutive quarters are counted as an accounting period, regardless of whether or not there are sales.

Nine major changes to the VAT Law.

State Administration of Taxation Announcement No. 2 of 2026:

① Maintain the previous rolling 12-month or 4-quarter standard for calculating whether cumulative sales revenue exceeds $5 million.

② The sales adjusted by the taxpayer due to self-supplementation or correction, wind control verification, and audit investigation shall be credited to [sales in the corresponding tax period] according to the time of occurrence of the tax obligation.

(iii) Those exceeding 5 million are required to register as general taxpayers within the next month's tax filing deadline (small-scale taxpayers have to pay attention to their income from time to time, and those exceeding the standard in the middle of the quarter can no longer wait for the quarterly filing before registering).

④ Key point! The effective date for general taxpayers is the 1st day of the period in which the required standard is exceeded (i.e., if the standard is exceeded mid-quarter, the tax is calculated at 13% for the month in which it is exceeded! (No more waiting for quarterly filing before upgrading the general taxpayer).

⑤ If a general taxpayer is registered, the effective date of the general taxpayer is the 1st day of the period in which the registration is made (there is no next-month effective date! Only effective on the 1st of the current month!) The effective date of the general taxpayer registration is the 1st day of the period in which the registration is made (there is no next month effective date!

⑥ If the effective date has been declared as a small-scale taxpayer for VAT, the taxpayer shall correct the declaration on a period-by-period basis according to the general taxpayer (late registration as a general taxpayer? No matter, correct and pay 13% VAT from the month of exceeding as general taxpayer).

(vii) Highlights! Taxpayers for the fourth quarter of 2025 or December tax period small-scale taxpayers VAT declaration, annual VAT sales exceed the prescribed standards, the effective date of the general taxpayer for January 1, 2026 (the last quarter of 25 years exceeded the 5 million, do not worry, but also in accordance with the old method from January 2026 will be recognized as a general taxpayer).

⑧ Highlights! Due to self-supplementation or correction, wind control verification, audit checks and other adjustments to the sales of 2025 and before the tax period, the annual assessable value-added tax sales in excess of the required standard, the effective date of the general taxpayer is not earlier than January 1, 2026 (26 years ago, omitted to declare and has exceeded the 5 million how to do? (Don't worry, the previous corrections are still on a small scale, but those after 2026 will have to pay 13% VAT back as a general taxpayer).

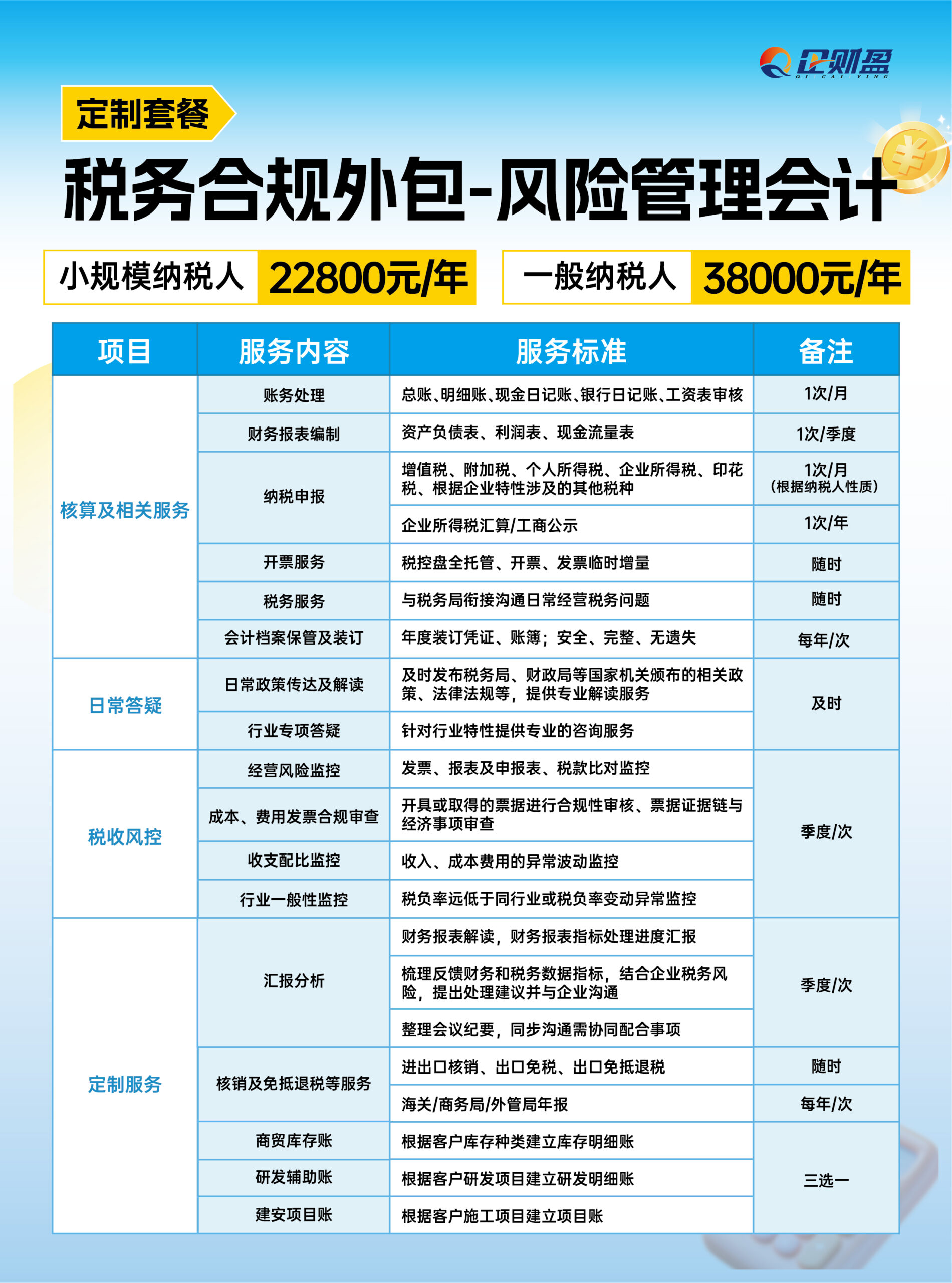

⑨ Stop the general taxpayer counseling period management requirements. If you encounter corporate tax compliance issues, you can refer to Enterprise Finance Group's Tax Compliance Product Package I to solve tax compliance or difficult account processing, etc., you can always consult (WeChat same number: 13045886252)▼▼▼

02 Impact Profiling, Triple Stress for Cross-Border Sellers

The new tax law creates a triple pressure on cross-border sellers, each of which has a direct impact on the profit margins and operating model of the enterprise. The direct squeeze on profit space is the most intuitive impact. After cross-border e-commerce sellers switch from small-scale taxpayers to general taxpayers, the tax rate will jump from 1% or 3% to 6% or 13%.

If it is not possible to obtain compliant VAT invoices from suppliers for input credits, the tax burden will increase significantly.

A tax expert pointed out, "The past model of choosing 'non-invoicing' suppliers in order to save costs will directly cannibalize corporate profits under the new regulations." The increased complexity of financial accounting and data matching is the second pressure.

The data reported by cross-border e-commerce platforms to the tax authorities is usually "gross revenue" including refunds, taxes and fees, while domestic tax declarations need to be based on "net revenue" calculations.

This difference in data caliber could lead to sellers incorrectly triggering the general taxpayer standard or risking inconsistent tax accounting. The centralized exposure of historical compliance risks is a constant wake-up call for sellers.

The retrospective mechanism in the new tax law makes any undeclared income in the past a "time bomb". A medium-sized cross-border e-commerce business owner said frankly: "We are now most worried about those who received money through personal accounts a year or two ago, according to the new regulations, if they are found out, not only do they have to pay back the tax, but also calculated according to the tax rate at that time, the cost is too high."

If you encounter more difficult corporate tax compliance issues, you can refer to Enterprise Finance Group's Tax Compliance Product Package II to solve them, and you can consult with us at any time (WeChat same number: 13045886252)▼▼▼

03 Coping strategies, a four-step survival strategy for cross-border e-commerce companies

In the face of the challenges posed by the new tax law, cross-border sellers can adopt a four-step strategy to effectively respond:

Step 1: Immediate self-examination and establishment of a dynamic monitoring system.Sellers should immediately review their cumulative revenue for the past 12 consecutive months or four quarters to accurately determine if they are close to the $5 million red line.

It is recommended to use professional financial software or ERP tools to set up sales early warning function to provide early warning of the risk of reaching the target. You can consider monthly and quarterly fixed time for revenue accounting to avoid being passive.

Step 2: Completely upgrade the supply chain compliance system.Review key supplier qualifications on a case-by-case basis to ensure that they canIssuance of compliant VAT invoices.. Clarify tax clauses in purchasing contracts by including requirements for invoicing type, rate, point in time, etc., and incorporate tax costs into purchasing decisions.

An industry veteran suggests:"Tax compliance in the supply chain must now be a core consideration, not just price and quality."

Step 3: Build a comprehensive and standardized accounting system.Ensuring the unity of business flow, contract flow, invoice flow and capital flow is the basis for dealing with tax verification. Stop high-risk operations such as the use of personal accounts to collect payments, conceal income and arbitrarily split subjects.

Step 4: Actively study the utilization of preferential policies.In-depth understanding of tax exemption and refund policies related to cross-border e-commerce exports, such as the "9810" overseas warehouse model. Turn compliance costs into a long-term competitive advantage rather than simply a burden.

Tax compliance has become a global norm, not just at home, the European VAT system has seen regulation soar in the last two years, as can be seen from the recent large number of Italian tax codes being investigated leading to invalidations, compliance is the sustainable force for long term business development.

If you encounter particularly difficult corporate tax compliance issues, you can refer to Enterprise Finance Group's Tax Compliance Product Package III to solve them. If your company needs tax compliance or more difficult account processing, etc., you can always consult (WeChat same number: 13045886252)▼▼▼▼

04 Cross-Border Tax Compliance: 2026 Survival Guide for Cross-Border Sellers

1) Supply chain reshaping: from price-oriented to tax-health-oriented The financial director of a cross-border apparel company in Guangzhou has made a calculation: if you only consider the purchase unit price and ignore the tax compliance of the supplier, you may not be able to obtain a compliant input invoice and pay more VAT, and the actual cost will be higher by 3-5 percentage points. After 2026, supplier selection criteria will have to be weighted towards "tax compliance". Sellers are advised to initiate supplier screening immediately to ensure that all purchases can be invoiced with VAT compliance.

2) Pricing strategy adjustment: tax costs must be internalized Hangzhou, a home furnishing category hypermarket has adjusted its pricing model in advance: "We have fully internalized the cost of VAT into our product pricing, which may affect competitiveness in the short term, but avoids tax risks in the long term." With the new law in place, price wars will have to consider tax compliance costs. Business models that appear to be low-priced but fail to provide tax compliance credentials will be unsustainable.

3) Overseas warehouse tax treatment needs to be clarified to avoid double taxation Mr. W, a seller on the European site, shared his experience, "We have re-planned our logistic path to ensure that the tax treatment in each step meets the requirements of the new law. Especially the movement of goods in overseas warehouses now requires clearer documentation on tax handling."

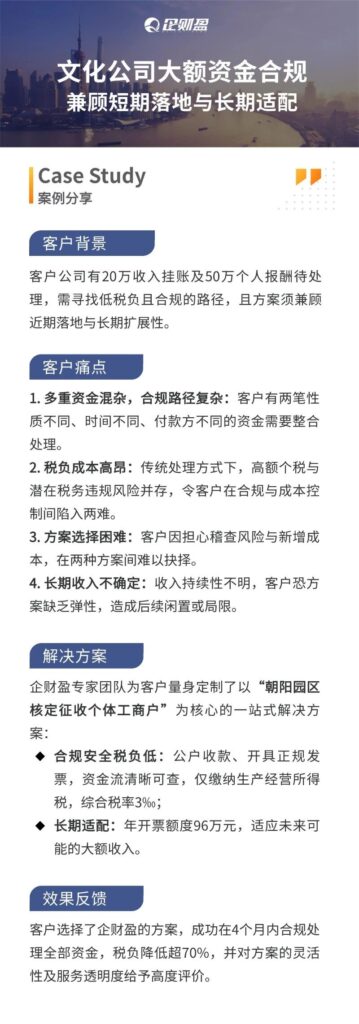

There is also a children's clothing e-commerce enterprise that moved to Guangzhou from a mainland city, which is a real customer case of our Enterprise Caiying, selling through Amazon and TIKTOK platforms, with an annual turnover in the order of ten million dollars.

Although the enterprise is profitable, there are hidden problems in fiscal compliance for a long time - the store operates as a domestic individual household, borrowing the name of another person to register, and it is difficult for the actual operator to dock the tax verification, while there is a large number of lack of cost tickets in the business, and the tax risk is increasingly prominent.

Despite the busy business and cross-regional operations, the core decision makers of the enterprise have a clear understanding of compliance and tax security.

They are eager to systematically avoid risks and control the tax burden, and look forward to a professional and efficient team to help cope with all kinds of unexpected financial and tax problems, so they find us to cooperate with Enterprise Caiying.

This cooperation not only solves the momentary needs, but also reflects the deeper needs of cross-border e-commerce enterprises for professional financial and tax accompaniment in the new economic environment - what they need is not only the program, but also the reliable experts and the support that can be landed, which is exactly the value of the service that we, Enterprise Caiyin Group, continue to build.

If you plan to register a U.S. company/Singapore company/Japanese company/Thailand company/Malaysia company/Canada company/Mexico company/Brazil company/Britain company/France company/New Zealand company/Japanese company/Singapore company/Vietnamese company/Indonesia company/Dubai company and other foreign companies registered in the relevant business and financial services, or plan to register a Hong Kong company/Shenzhen company/ Guangzhou company / Shanghai company / Hangzhou company / Beijing company / Hainan company and other domestic companies registered business services, the company's annual audit audit / bookkeeping tax / payment of MPF / change of information / bank account / ODI record / BVI registration / tax compliance / cross-border e-commerce accompanied by running on behalf of the operation of the enterprise one-stop service, you can add my WeChat (phone with V: 13045886252) at any time to consult ↓↓ ↓

05 A real case of tax compliance for the Enterprise Finance Group

06 Choose Enterprise Caiying Group for long-term cooperation

🏆 Why choose Enterprise Finance?--More than bookkeeping and tax preparation, we are your "tax architect" and "risk prevention and control expert".

Since its establishment, Enterprise Caiying has accompanied the growth of 300,000+ enterprises. With the mission of "empowering every entrepreneurial dream", we focus on providing SMEs and entrepreneurs with one-stop financial and tax solutions, including "pain point diagnosis, compliance structure, tax optimization, and continuous accompaniment".

Our professionalism stems from deep industry experience and full-service support:

✅ Know business, know more about risk: we go deep into the operating scenarios of different industries, diagnose the pain points of finance and taxation from the business flow, and provide landable compliance transformation programs.

✅ Full License Qualification Guarantee: With the professional qualification of CPA firm, the team is composed of senior tax accountants and accountants to ensure the legal compliance of the program.

✅ One-stop solution: transform high-frequency pain points (e.g. lack of tickets, social security, public-to-private transfers) into standardized product modules, balancing efficiency and customization.

✅ Long-term accompanying service: not only solving the current problems, but also focusing on the financial and tax planning in the growth cycle of the enterprise, helping sustainable development.

🔍 Our service logic: from "Risk Identification" to "Architecture Reinvention".

In-depth diagnosis: not only look at the statement, more in-depth business flow, contract flow, capital flow, locate the root cause of risk.

Comparison of solutions: We insist on "data speak", clearly presenting the tax burden, risk and cost under different paths, helping clients make rational decisions. Transparency in the whole process: We proactively explain the cost, process and cycle, so that customers can have peace of mind and control in the whole process.

Long-term adaptation: We provide scalable and sustainable tax and financial structure suggestions according to the development stage and future planning of the enterprise. Tax compliance is not a cost, but a "safety belt" and "gas pedal" for enterprises to move forward.

Choosing a partner who understands both policy and business can help your organization walk down the compliance path with more ease and confidence.

statement denying or limiting responsibility

Image source: some of the image material in this article from the network, such as copyright issues, please contact us to replace the deletion of processing.

Information reference: The content of this article is synthesized from the internal materials of Enterprise Caiying and relevant public network information.

Content Editor: This article was edited and designed by the Operations Department of the Enterprise Caiying Group.

Warm reminder: The relevant policies, conditions, time limits, fees and other information described in this article may be subject to dynamic adjustments, please refer to the latest official announcements or the actual application of the specific circumstances prevail.

Tags:

Tax Compliance Guide

Tax Compliance Cases

Corporate Tax Compliance

tax planning

taxation services

Tax Compliance

Recommended

Cross-border e-commerce B2B must see! Registered Hong Kong company stationed in the Ali International Station, really fragrant!

In today's globalized business environment, the cross-border e-commerce B2B model is rapidly emerging with its unique advantages. For many enterprises engaged in cross-border trade, choosing a suitable platform and registering an advantageous company are undoubtedly the key keys to open the door to the international market.

2024 Hong Kong Company Account Opening Tips! How to choose the right Hong Kong bank account?

Global anti-money laundering regulations are becoming more and more stringent, the banks to maintain an account of the sunk cost is getting higher and higher, not moving hundreds of millions of dollars in fines, so that the major banks to open an account threshold as well as the audit process high up, already have a Hong Kong company bosses, how to choose the Hong Kong bank to open a public account? How much does it cost and how to operate? Today to give you a detailed introduction to the Hong Kong company account how to choose, as well as the approximate costs required and other content.

Hong Kong company registration advantages + registration conditions + registration process to share!

If you want to start a business and develop overseas markets, registering a Hong Kong company is undoubtedly a very forward-looking choice. With its unique geographical location, sound legal system, low tax rate and open business environment, Hong Kong company has become a "sharp weapon" for many business owners to open up overseas markets. Why is it so important to register a Hong Kong company in 2024?